Year-End Supply Chain Review: What Actually Mattered in 2025

Global Supply Chains in 2025: Stability Delayed, Not Delivered

2025 did not deliver normalization. It delivered a transition into a new operating baseline shaped by geopolitics, energy exposure, and structural demand shifts. Trade flows remained intact, but efficiency, predictability, and cost discipline did not fully return.

The system functioned. It did not stabilize.

Maritime Trade: Rerouting Became Structural

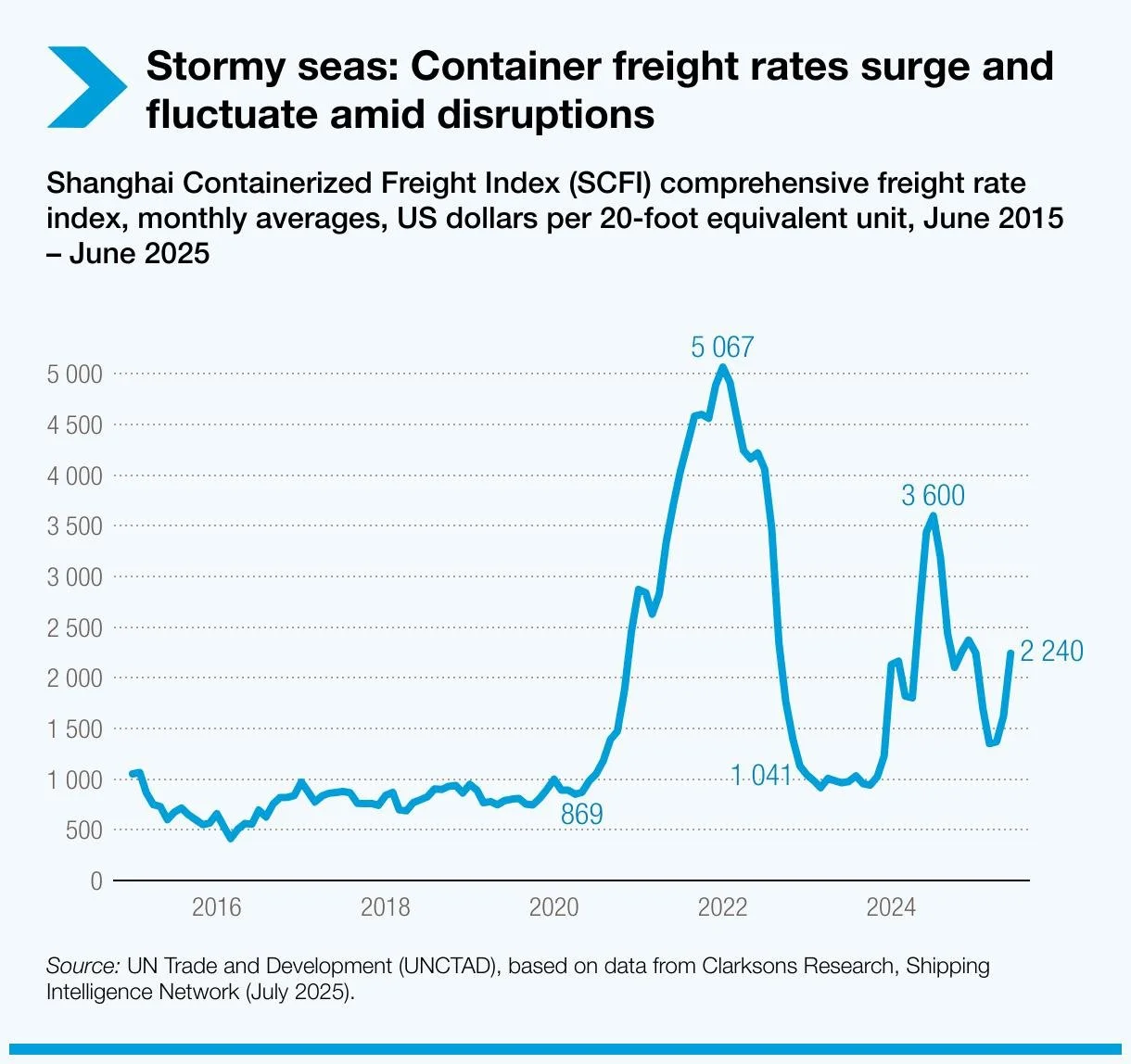

The most visible impact came from shipping. Continued security risks in the Red Sea forced carriers to avoid the Suez Canal for most of the year, redirecting vessels around the Cape of Good Hope.

• Asia to Europe transit times extended by 10 to 20 days

• Vessel capacity tightened due to longer route cycles

• Freight rates stayed elevated relative to historical norms

Earlier in the year, Panama Canal restrictions reduced daily vessel transits due to water constraints, further tightening global routing flexibility.

Net effect:

Global shipping capacity was not reduced in absolute terms, but it became less efficient, increasing cost per unit moved and reducing schedule reliability.

Trade Policy: Controlled Globalization

Trade in 2025 was increasingly shaped by policy rather than pure economics.

• Export controls on advanced semiconductors and AI technologies remained in place

• Tariff frameworks across the U.S., EU, and China continued influencing sourcing decisions

• Retaliatory measures, including restrictions on rare earth exports, impacted material flows

Net effect:

Globalization did not reverse, but it became conditional. Trade execution required alignment with regulatory frameworks, increasing lead time, and compliance overhead.

Energy and Fuel: Cost Floor Reset

Energy markets avoided extreme spikes but remained structurally elevated.

• Oil prices fluctuated within a controlled band, driven by geopolitical signals and supply management

• Extended shipping routes increased bunker fuel demand

• Energy-intensive manufacturing sectors operated under sustained margin pressure

Net effect:

Energy costs established a higher operating floor, directly impacting logistics and production economics.

Agricultural Trade: Rebalancing Supply Corridors

Agriculture emerged as a key variable in global supply stability.

• China diversified soybean imports between the U.S. and Brazil

• Weather variability in South America affected crop yield and export timing

• Logistics constraints in key export regions disrupted grain flows

Net effect:

Commodity supply chains became more dynamic, influencing pricing across food, chemicals, and industrial inputs.

Critical Materials: Strategic Constraint

Material concentration risks translated into operational constraints.

• Rare earth export controls impacted automotive, electronics, and defense sectors

• Lithium and battery supply chains remained tightly linked to geopolitical positioning

• Base metals stabilized but did not return to pre-disruption pricing levels

Net effect:

Raw materials transitioned from procurement inputs to strategic assets, influencing long-term sourcing and investment decisions.

Manufacturing Footprint: Expansion Over Relocation

Production networks did not shift from one region to another. They expanded.

• Continued investment into North America driven by policy incentives

• Growth in manufacturing capacity across India and Southeast Asia

• Persistent reliance on China for scale and capability

Net effect:

Supply chains became geographically broader but operationally more complex, increasing coordination cost.

Semiconductors and AI: Demand Reallocation

The semiconductor market moved into a bifurcated state.

• Standard chip availability improved with capacity expansion

• AI-driven demand concentrated supply in high-performance segments

• Capital and production shifted toward advanced nodes and memory

Net effect:

Shortages did not disappear. They became segment-specific, impacting downstream industries unevenly.

Macroeconomic Signals: Growth Without Momentum

Manufacturing indicators reflected limited expansion.

• Global PMI hovered near neutral expansion levels

• Purchasing activity remained cautious

• Inventory strategies avoided aggressive buildup

Net effect:

Demand persisted, but confidence remained constrained, limiting scale acceleration.

Conclusion: A System Defined by Structural Friction

2025 marked the transition from episodic disruption to structural friction.

Shipping inefficiencies, policy-driven trade, energy cost floors, material constraints, and uneven demand recovery collectively reshaped supply chain dynamics.

No single event defined the year. The accumulation did.

Supply chains remained operational, but at a higher cost, longer lead time, and increased complexity than pre-disruption norms. That is the new baseline!! Level UP!